Watching the Economy by Clint Burdett CMC® FIMC

"In With The New January Predictions" updated August 2011

In mid-January 2011, I picked two very skilled commentator's "predictions" and observations of economic conditions in 2011. Their observations are below, and in July 2011, I think still on the mark. First, my big picture observation early July remain the same - aggregate demand has leveled off or is slightly declining. I'm updating their comments in red.

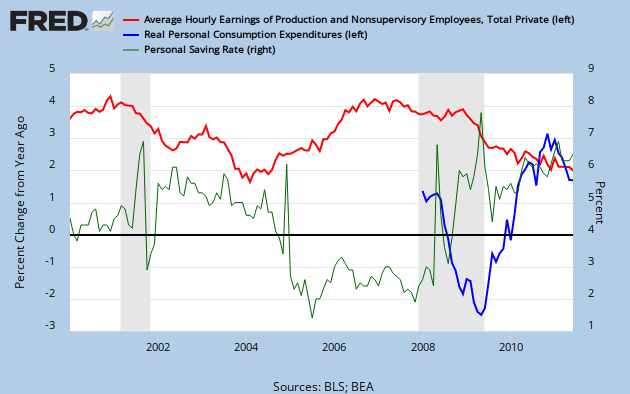

Sustained SP500 rallies are supported by improving real Personal Consumption Expenditures compared to the past year (wallets opening - the blue line - a proxy for societal demand) and declining Average Hourly Earnings compared to last year (confidence in the future, raises coming - the red line).

If the initial SP500 rally mid-2009 to date (green line) is not just a "we're glad the GR is over" plus inventory replacement one, then continued decline of Average Hourly Earnings growth compared to the last year (red line) is not a good sign for the US economy, since real hourly earnings are the engine of PCE improvements (green line). Compared to last year, folks are increasing their spending at greater than 2% but underlying salaries are not growing in line with spending.

But now, large firms are borrowing at incredibly low rates giving them an edge, perhaps reflected in the continued SP500 rally (see Mark Carney, Governor of the Bank of Canada last point below).

By August , note that the year on year percentage change of real Personal Consumption Expenditures is tapering off indicating that consumers are cutting back again and over two years after the GR ended (NBER call), the SP500 has not reached it pre-GR levels. It is going to be a slow go ...

(Interval Quarters - click graph to open StLouisFed FRED edit page)

Replace the SP500 with the Personal Savings Rate, which is trending down since the end of the Great Recession, to see conditions that do not suggest consumer demand is getting better: PCE (demand) down, average hourly wages (what we earn to spend) down , savings (setting aside reserves) down.

(Interval Quarters - click graph to open StLouisFed FRED edit page)

Mark Carney, Governor of the Bank of Canada in a December 13th 2010 speech to the Economic Club of Canada said:

Current turbulence in Europe is a reminder that the crisis is not over, but has merely entered a new phase. In a world awash with debt, repairing the balance sheets of banks, households and countries will take years. As a consequence, the pace, pattern and variability of global economic growth is changing, and Canada must adapt. (July 2011 - correct)

For the crisis economies, the easy bit of the recovery is now finished. Temporary factors supporting growth in 2010–such as the turn in the inventory cycle and the release of pent-up demand–have largely run their course. Fiscal stimulus is turning to fiscal drag and, for some countries, rapid consolidation has become urgent. Household expenditure can be expected to recover only slowly. This all implies a gradual absorption of the large excess capacity in many advanced economies. (July 2011 - correct)

This is not surprising. History suggests that recessions involving financial crises tend to be deeper and have recoveries that take twice as long. In the decade following severe financial crises, growth rates tend to be one percentage point lower and unemployment rates five percentage points higher. The current U.S. recovery is proving no exception.

In such an environment, very low policy rates in the major advanced economies could be in place for a prolonged period–a possibility underscored by the recent extensions of unconventional monetary policies in the United States, Japan and Europe. (Bernanke July 12th hints at QE3.)

This tendency towards low-interest rates is being reinforced by structural forces. The global economy is rapidly becoming multi-polar, with emerging-market economies now driving commodity prices, representing almost one-half of all import growth, and accounting for about two-thirds of global growth. (July 2011 consumer demand is not increasing in mature economies.)

|

He then warns about complacency about low interest rates since healthy economies grow with about 2.0% annual inflation. With low short and long term rates, businesses tend to not enforce best practice and increase their risk when the economy starts to expand. His speech is well worth the read.

Reinhart and Reinhart (Aug 2009) point out that housing cycles are longer in duration than the equity market cycles and are intimately connected with a multi-year credit cycle. Worldwide, expect housing prices for at least ten years to be about 15 to 20% below their peak before the Great Recession.

A credit boom that precedes a credit shock takes at least one decade to build, and deleveraging takes as long. The US at Q1 2010 has deleveraged about 20% of GDP (credit/GDP) of its private debt from late 2007, mostly in housing.

So it ain't over ... and, it may get worse into the fall of 2011.

David A. Rosenberg from Gluskin Sheff said about the 2011 human nature risks, my term:

- Market sentiment in early 2011 is as overly optimistic now as it was pessimistic at the July August 2010 lows. (July 2011 - NOT correct - investors like lean, mean earnings machines.)

- Eurozone fiscal deflationary shock. (July 2011 - correct)

- Anti-inflation policy restraint in emerging Asia. (July 2011 - correct)

- Widespread cutbacks at the state and local government level. (July 2011 - correct)

- Debt ceiling issue triggers major rounds of market volatility. (Aug 2011 accurate)

- Tax breaks that are temporary tend to have marginal economic impact with few multiplier impacts, hence GDP revisions will likely be to the downside post-Q1. (July 2011 - correct)

- Another downleg in home prices undercuts confidence and spending (with around two years’ supply of total vacant inventory backlog). (July 2011 - correct)

|

In early June , many indicators are reporting a slowing pace as Rosenberg predicted. See Econobrowser - Jim Hamilton at UCSD and Minzie Chinn at U of Wisconsin Madison -at http://t.co/mub2yZz

You may not reprint this article for sale without my expressed written permission.

You may post or reprint this article to educate as long as you credit my work

and provide a link to www.clintburdett.com

|

|