Inflation to Remain Tame - Pace of Recovery Might Pick Up Later This Year

[CB: Updated 3/11 to include comparison of federal to all government sector employees (local, state and federal)]

March 7, 2013

Compared to other financial crises worldwide, the US is doing surprising well but from such a deep drop, there is still a long way to go as housing construction adds steam to the recovery. Pending Federal furloughs and program cuts may not slow us down.

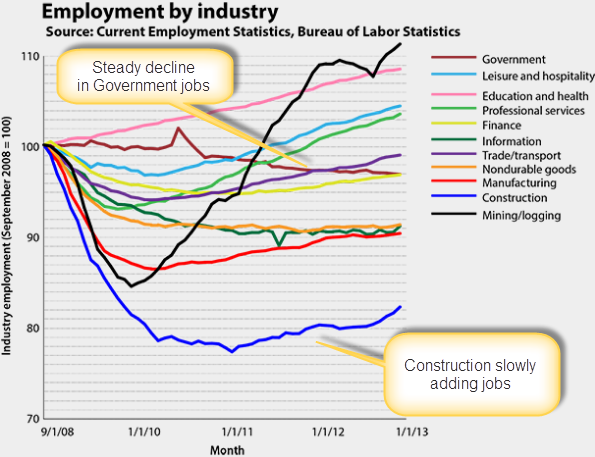

The March 8 Jobs Report shows construction is improving, slowly adding jobs. New and Existing Single Family Housing inventory are declining and may bottom this year.

In good times, housing contributes about 18% to GDP. In bad times, it has been closer to 15%. Will first time home buyers show up as mortgage rate remain low?

Long term trend of declining average hourly wages continues and high unemployment will hold down inflation.

Average Hourly Earnings decline has been a significant drag for years, it reduces the funds families have to spend.

(Click to go to StLouisFed FRED graph editor)

Finally, we see the first up tick four consecutive months.

(Click to go to StLouisFed FRED graph editor)

Do Federal layoffs matter at this point in the recovery?

I suspect that the "chess masters" in our political debate see other sectors job growth offsetting continued losses in the Government sector (local, state and federal employees ex-military) in this chart.

Source: Wonkblog

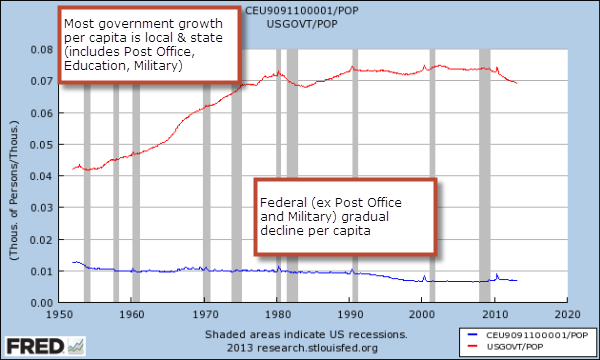

The next chart compares growth of the Federal component to all government sector employees in the US. (The 10 year repeating spikes are for Census temporary hiring.)

Keeping the Big Government - Small Government debate (nee culture war) in mind, the substantive growth in the local, state and federal government per capita (total government employees divided by the total US population) was from 1953 to 1979 (0.042 to 0.074).

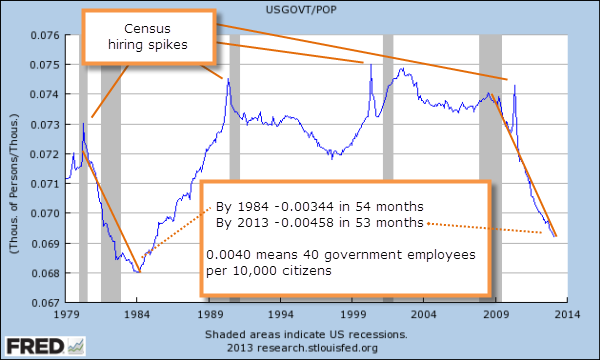

The 1980 and 2008 recessions triggered two reductions as the number of government sector employees as per capita that had stayed in a narrow range (0.068 to 0.075) since 1979.

In February 2013, there were 21,525,000 people employed in the government sector (including Post Office and education) and 2,134,000 Federal Government Employees (ex-Post Office).

Click to see the chart and data on St. Louis FED FRED Database

The number of all government sector employees (from the above chart enlarged) has been declining since at a slightly higher rate per capita (slope of line is steeper) than it did from 1979 to 1984. Since 2008, 706,000 government sector jobs have been cut to February 2013.

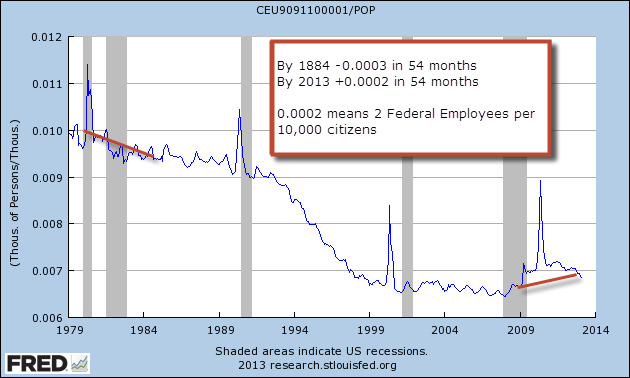

Honing in on just the Federal sector for the same time period (note that y axis starting point and range shift; ex Post Office) there was a decline by 1984 and in increase by 2013.

Furloughs of Federal employees can range from forced unpaid days off each month to loss of a job (a layoff which takes a least four months given job protections).

If the sequester budget cuts impact are significant and furloughs become Federal layoffs, that will extend the reductions to the most dramatic cuts in government sector employees per capita since WWII. But the Federal Government sector is only 10% of the total government sector and local and state layoffs have tapered off significantly.

Recovery to accelerate maybe. Maybe not ...

Will these Federal budget cuts (including layoffs rather than a few forced days off per month) trigger another recession? It does not appear layoffs will since the numbers are too small. Other outlays, hard to know until it happens.

CBO estimates the sequesters impact as a 0.6% drop in GDP where historically we could see a 2% to 3% increase in GDP from housing in 2014.

|